Hello, my name is Bhuvan, and thanks for reading What the hell is happening?

This newsletter is deliberately messy. It's more of a permanent draft than a finished post. There are no conclusions, and if there are any, they're unintentional—because nobody has any idea what's happening in the world. Think of this as a frantic attempt to make sense of the unfolding chaos.

The law of unintended consequences

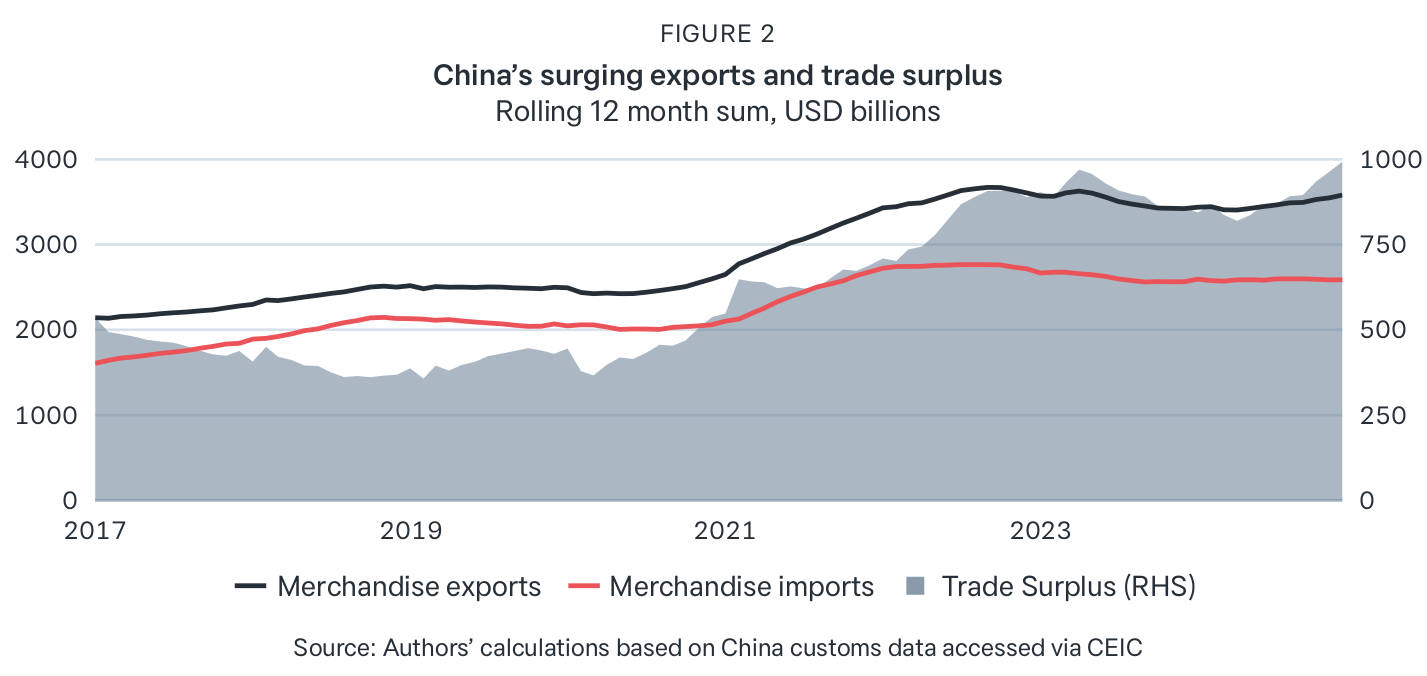

When you are talking about things that are happening in the world, there’s China and the rest of the world. The scale at which China operates is so massive that it dwarfs the rest of the world. Nowhere is this truer than in trade.

China runs a $1 trillion trade surplus with the rest of the world. That’s insane. No other country has ever managed to do what China has done with manufacturing in the history of humanity.

But with US tariffs on Chinese exports still at 40% even after the pause of the trade war, there are signs that Chinese exports to the US seem to be falling. We don’t know the full extent of the damage yet. Now, considering China consumes very little, all the goods that would’ve gone to the US have to go elsewhere.

The challenge of China’s export-oriented economic model is this: 32% of the world’s manufacturing emanates from China, but only 12% of global consumption is China-based. This imbalance between production and consumer demand creates an over-supply of goods in the Chinese economy, which is exported into international markets. This in turn creates a major trade surplus which, in 2024, was nearly US$1trn. - Deutsche Bank

Lowy Institute

That’s exactly what’s happening. Chinese exporters are now redirecting their goods everywhere from Europe, Britain, to Latin America:

Today, a new China shock is cascading across the globe from Indonesia to Germany to Brazil.

As President Trump’s tariffs start to shut China out of the United States, its biggest market, Chinese factories are sending their toys, cars and shoes to other countries at a pace that is reshaping economies and geopolitics.

This year so far, China’s trade surplus with the world is nearly $500 billion — a more than 40 percent increase from the same period last year. — The New York Times

Official data from both nations point to a pick-up in the value of Chinese exports to the UK after the US president slapped hefty duties on products from the world’s second-largest economy before recently reducing them. Exports of small parcels and electronics have jumped in a sign of possible rerouting to avoid the US tariffs.

The figures add to evidence that as Trump’s trade barriers reduce the US’s reliance on Chinese production, demand for those exports often shifts elsewhere rather than disappears. — Bloomberg

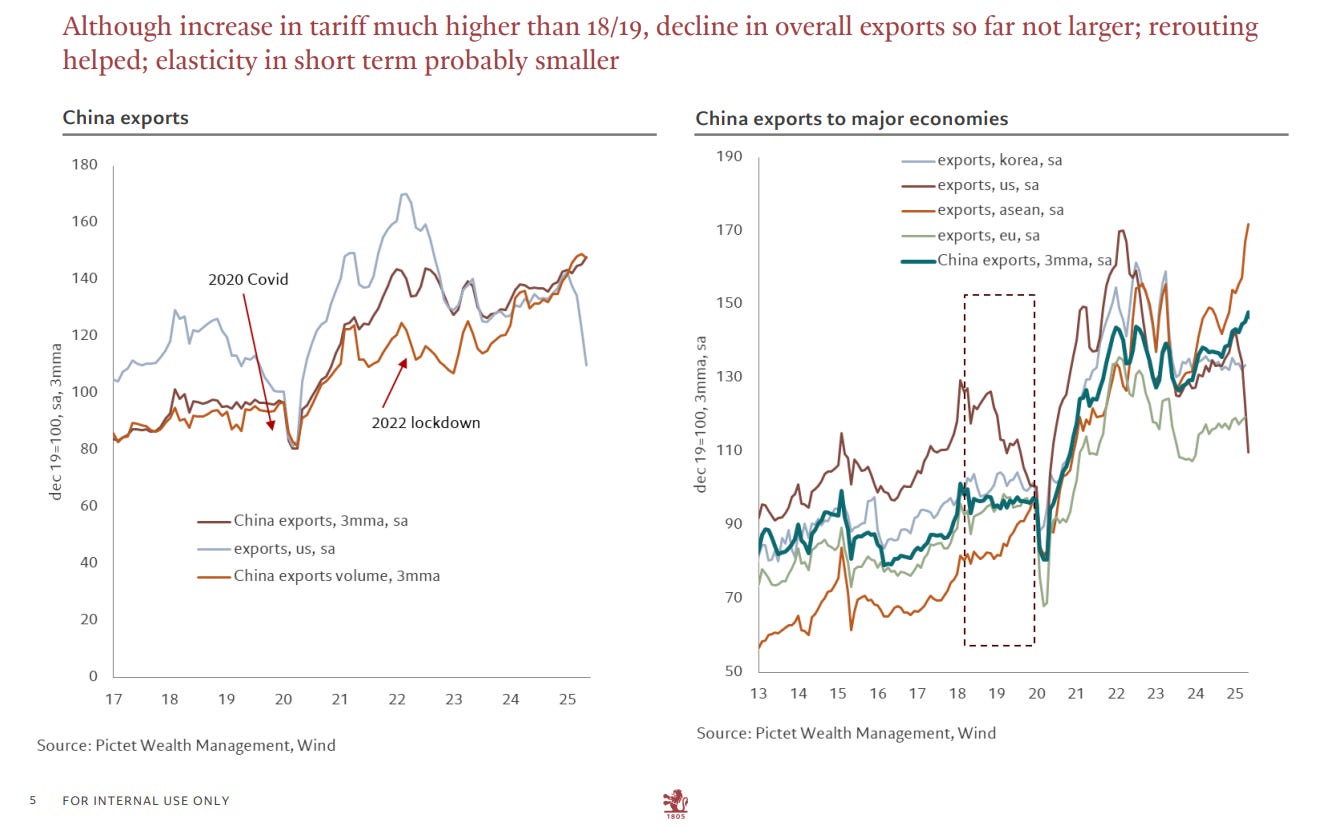

Two things seem to be happening simultaneously. On the one hand, China is trying to reduce its export dependency on the US and diversifying across Africa and Asia.

At the same time, there is some evidence that Chinese exporters are using backdoor entries to the US through Thailand, Vietnam, etc.

Companies are trying to mitigate the impact of the trade war by rerouting: China is exporting more to ASEAN and Latin America, which in turn are also exporting more to the US. In recent months, Chinese direct exports to the US experienced a sharp decline, falling by -21% y/y in April and -35% in May 2025 (compared with +5% y/y in Q1) – even though total Chinese exports continued to grow (+8% y/y in April and +5% y/y in May).

Notably, Chinese exports to ASEAN, India and Latin America accelerated in April and May, respectively growing on average by +18%, +17% and 10% y/y. In the meantime, Vietnamese exports to the US grew by +34% y/y in April and +41% y/y in May (after +22% y/y in Q1). Similar outperformance can be observed in US-bound exports from Taiwan (+87% y/y inMay) or from Brazil (+11% y/y), suggesting that some rerouting of Chinese exports might be at play.

As a result, China’s trade surplus with ASEAN and Latin America increased to USD31.5bn in May 2025 (compared with USD19bn on average in 2024), while the US trade deficit with these regions widened further to USD36bn in April 2025 (compared with USD29bn on average in 2024) – see Figure 5.

Trade is like water; it always flows somewhere else.

Just because China wants to export doesn’t mean countries will welcome Chinese exporters. Take the case of exports of Chinese EVs; the flood of exports into Brazil is triggering a backlash there:

Brazil has emerged as a flashpoint in the China auto industry's torrid global expansion. A growing surplus of new cars being pumped out of Chinese factories has led to an export boom over the past five years, helping China pass Japan in 2023 to become the world’s top vehicle exporter. Much of this excess is being shipped overseas, to markets like Europe, Southeast Asia and Latin America. — Reuters

This mirrors the broader trend of countries raising trade barriers against a whole range of Chinese exports:

MERICS

What’s the solution to all this? Here’s Sander Tordoir, Chief Economist at the Center for European Reform:

The EU and China are both trade-surplus blocs: They rely on external demand and need buyers, not sellers, as the United States reduces its demand. China will not act as a buyer: It suffers from anemic demand and continues to rely on net exports to grow its economy. It may offer to drop tariffs on EU imports, but many of its markets are burdened by overcapacity, which means European firms cannot export profitably. The only meaningful offer China can make is to stimulate its domestic consumption.

For as long as I can remember, there have been allegations that Chinese GDP numbers are useless and often overstated. Are they? Not according to a recent note from the US Federal Reserve. Some highlights:

Since the pandemic started, official Chinese GDP growth has closely followed other indications, which means that the most recent numbers are not too high. This is a change from before the pandemic, when official data seemed to be too smooth.

Even though COVID caused problems at first, industrial production was higher than pre-pandemic trends. This has helped make up for big drops in residential construction (down 40%) and property sales (down 70%).

From 2020 to 2024, net exports added more to GDP growth than in any other five-year period since the Global Financial Crisis. Strong demand for Chinese goods around the world during the pandemic has been a big reason for recent success.

Biotech revolution

It’s not just renewables that China is dominating; its biotech industry is also seeing a renaissance.

Five years ago, U.S. pharmaceutical companies didn’t license any new drugs from China. By 2024, one-third of their new compounds were coming from Chinese biotechnology firms.

In most cases, Chinese firms are not discovering new biological targets, nor are they crafting genuinely novel compounds to engage these targets through homegrown Chinese research. Instead, they piggyback on Western innovations by scouring U.S. patents, zeroing in on biological targets that are initially uncovered in American labs, and then developing “me too” drugs that replicate American-made compounds with only superficial tweaks, or producing “fast follower” drugs that capitalize on the original breakthroughs while refining key features to try to surpass U.S. innovation.

Facing fewer regulations, the Chinese drugmakers can move more quickly than U.S. biotechnology companies — synthesizing copy-cat drugs based on our biological advances and then promptly moving these Chinese-made compounds into early-stage clinical trials, outpacing their American counterparts.

China’s government identified biotech as a strategic priority nearly two decades ago. But it was not until 2015 that things really took off, after the drug regulator launched ambitious reforms. It took on more staff and cleared a backlog of 20,000 drug applications in two years. Clinical trials were streamlined and brought into step with global standards. A study by Yimin Cui of Peking University and colleagues found that the time taken to approve the first round of human trials fell to 87 days, from 501 days before the reforms.

The changes coincided with a wave of returning “sea turtles”, the term for Chinese people who studied or worked abroad. China’s vast domestic market helped to attract big drugmakers to its shores, bringing know-how and talent. Easier listing rules gave biotech investors a clearer path to exit. Private funding for Chinese biotech firms rose from $1bn in 2016 to $13.4bn in 2021.

Chinese companies have established global clinical and commercial leadership in hematology oncology therapeutics, including Carvykti (a treatment from Legend Biotech in partnership with Johnson & Johnson for adult patients who have cancer of the bone marrow called multiple myeloma) and Brukinsa (a treatment from BeiGene for non-Hodgkins lymphoma). As a result, China has become a rich hunting ground for global pharma and biotech leaders looking to enrich their clinical pipelines, including AstraZeneca, Merck, GlaxoSmithKline, Johnson & Johnson, BioNtech, and more.3China went from contributing 4% of global biotech out-licensing deals to global pharma companies in 2019-2020 to 12% in 2023-2024, valued at $48 billion.

A new HIV prevention drug

In some fantastic news, the US FDA approved a HIV prevention drug by Gilead Sciences that represents a major breakthrough in the fight against HIV.

A summary of the drug from Perplexity:

Lenacapavir is a first-in-class HIV-1 capsid inhibitor, meaning it blocks the protein shell (capsid) of the HIV virus, preventing the virus from replicating and establishing infection in human cells.

Unlike current oral PrEP (pre-exposure prophylaxis) options that require daily pills, lenacapavir only needs to be given every six months, making adherence much easier for many people.

In large clinical trials (PURPOSE 1 and PURPOSE 2), lenacapavir showed ≥99.9% effectiveness in preventing HIV infection. Notably, in a study involving cisgender women in sub-Saharan Africa, zero participants who received lenacapavir contracted HIV.

It’s AI’s world; we’re just living in it

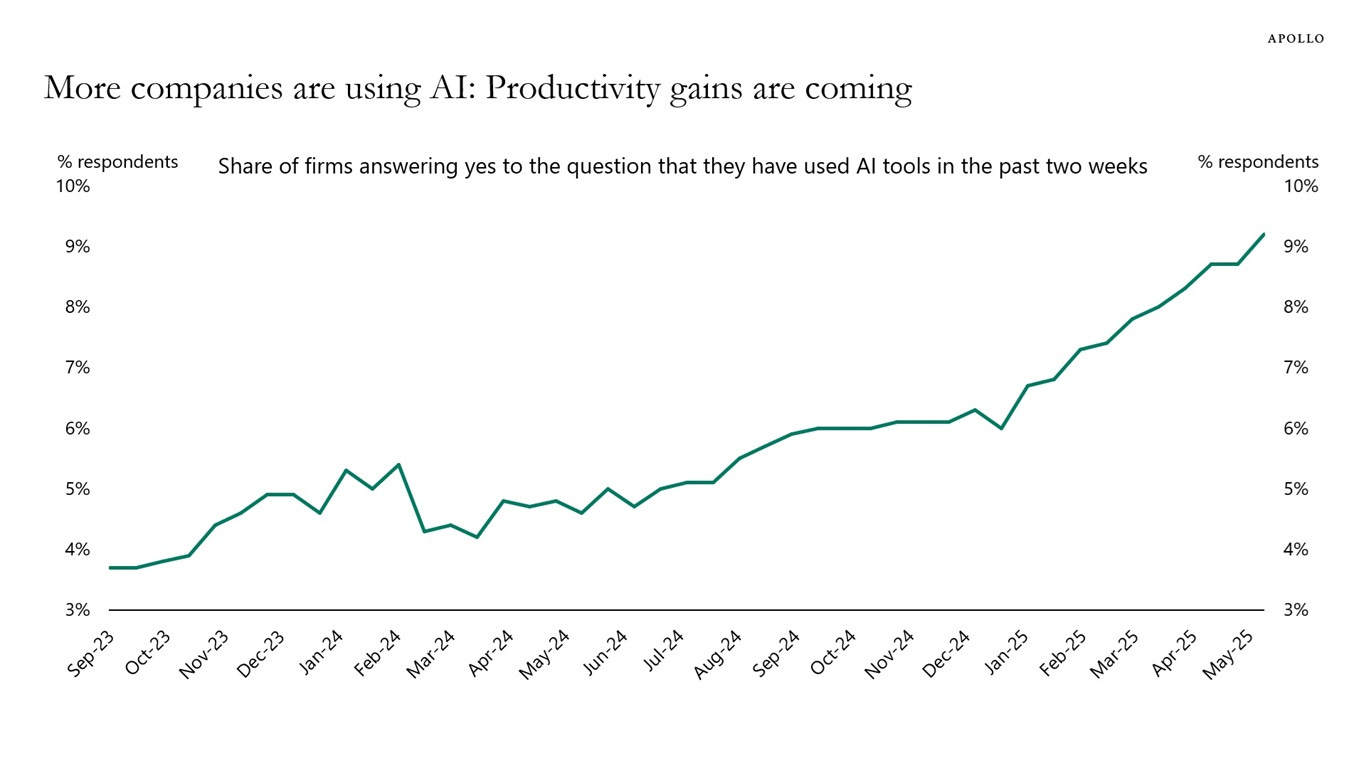

I obsessively try to follow the progress with AI because I’m operating under the assumption that it’s a monumental technological shift. Also, it might probably kill us. One key metric to watch out for is the rate of adoption, and there isn’t a whole lot of good data on it; all we have so far are spotty stats.

Here’s the latest data from a biweekly survey of 1.2 million firms on whether they are using AI. The adoption curve is breaking out on the upside.

Apollo

Then there’s the perennial question as to what will be the impact of AI on the economy and, by extension, our lives. As I wrote in the previous post, we don’t have a good answer because the technology is still new, adoption is low, and the rate of progress is quite high. However, as things stand, here’s a nifty summary from Allianz of various predictions on the impact of AI:

AI and productivity pressure in EU labor markets. The adoption of AI is expected to boost productivity by 10-30% across sectors, potentially raising global GDP by USD5-15trn by 2030. But these gains will take time to materialize and have not resulted in higher wages or broader welfare improvements so far. Routine jobs in knowledge industries are most at risk of displacement so company and employee adaptability will be key to job complementarity.

Economies heavily reliant on services will face these changes first, particularly in retail, professional services and the arts, with the labor share of income exceeding 70-80% and a sustained positive unit labor cost gap. This puts countries with high labor costs, such as Germany, France and Austria, under greater pressure to adopt AI to remain competitive, particularly compared to lower-labor-cost economies such as Italy, Poland and Spain.

Allianz

You can drive a high-speed train and a Boeing 787 through the dispersion in these estimates.

Like I wrote in a previous post, the entirety of the AI debate boils down to one question: Will AI take our jobs? It’s just been a couple of years since the launch of these AI tools and the adoption, like I mentioned above, is still not too widespread. So until the adoption rate is sufficiently high, we won’t have a clear idea about the impact of generative AI tools on jobs.

That said, there are some signs that these gen-AI tools are starting to take some jobs, especially in tech. Here’s a depressing story by

with first-hand accounts of employees in tech companies on how AI is leading to job loss, degradation, technical debt, and workplace toxicity:

I heard from workers who recounted how managers used AI to justify laying them off, to speed up their work, and to make them take over the workload of recently terminated peers. I heard from workers at the biggest tech giants and the smallest startups—from workers at Google, TikTok, Adobe, Dropbox, and CrowdStrike, to those at startups with just a handful of employees. I heard stories of scheming corporate climbers using AI to consolidate power inside the organization. I heard tales of AI being openly scorned in company forums by revolting workers. And yes, I heard lots of sad stories of workers getting let go so management could make room for AI. I received a message from one worker who wrote to say they were concerned for their job—and a follow-up note just weeks later to say that they’d lost it.

One way of measuring how good the current crop of large language models (LLMs) is to measure the length of tasks AI agents can complete. They are getting better, but can’t handle sessions for hours without an increase in error rates:

Current frontier AIs are vastly better than humans at text prediction and knowledge tasks. They outperform experts on most exam-style problems for a fraction of the cost. With some task-specific adaptation, they can also serve as useful tools in many applications. And yet the best AI agents are not currently able to carry out substantive projects by themselves or directly substitute for human labor. They are unable to reliably handle even relatively low-skill, computer-based work like remote executive assistance. It is clear that capabilities are increasing very rapidly in some sense, but it is unclear how this corresponds to real-world impact.

METR

State of the AI union

The awesome Ben Thompson published an interesting post looking at how the big 5 tech companies—Apple, Google, Meta, Amazon, and Microsoft—are positioned in the AI race. Here’s a quick summary:

Apple

Apple doesn’t have any cutting-edge models or is close to building one. At the moment, it’s entirely reliant on this partnership with OpenAI.

This isn’t an immediate threat to Apple because all the AI apps like ChatGPT and Claude run on phones, and Apple has a good phone.

Just like how Microsoft accepted that it lost the mobile race and pivoted to cloud, Apple should double down on building the best hardware for consumer AI applications.

Google

From chips to frontier models, Google is fully integrated and has some of the best infrastructure capabilities. It also has unique data advantages with search indexing, YouTube, etc.

It also faces one of the biggest threats because AI chatbots can disrupt its core search business model.

Google has taken this threat seriously and responded well by integrating AI into search while maintaining monetization, plus strong potential in cloud computing.

Meta (Facebook)

Meta’s Llama 4 model was disappointing, prompting Mark Zuckerberg to go into crisis mode and personally try to recruit hundreds of AI researchers.

This is a sign that Zuck perceives losing out on the AI race as a big threat to the core business model. AI should, in theory, help Meta’s core business through content personalization and ad targeting.

Having said that, Zuckerberg's "superintelligence" vision is vague, and the company seems to lack a coherent AI strategy.

Microsoft

The Azure cloud business will benefit significantly from AI demand.

The OpenAI relationship is frayed, but Microsoft still has significant leverage. Microsoft should focus on making investments in the likes of XAI, etc, to secure model access.

One threat to the Microsoft 365 business is the potential replacement of knowledge workers.

Amazon

AI is not disruptive to Amazon’s core business; if anything, it’s good because of increased demand for AWS.

Amazon’s partnership with Anthropic seems more stable than Microsoft-OpenAI and will drive increased usage.

Early investments in the Bedrock platform and Trainium chips provide future optionality.

A measured take on the future of AI

Benedict Evans is one of the most thoughtful commentators on technology. His take on the progress of AI is more sanguine and measured as opposed to the typical boomer/doomer takes on the topic.

We are sort of at the stage now of like the internet in the mid-'90s or mobile in the mid-2000s when it was very clear that this was going to be an enormous thing but it wasn't clear at all what the market structure was going to be, where the value capture is, what the building blocks are, how it all fits together, what it's going to look like.

And we're sort of at the same stage now, I think, in that you've got this thing that's amazingly cool but it's not clear how it works, it's not clear where the value capture is or the market structure, it's not entirely clear what you do with it. There's a bunch of people kind of running around with their hair on fire saying "Oh my god it's amazing, you don't get it, this is everything." And then you go and look at the survey data and you see that basically 75% of people in the developed world have looked at this stuff and 50% of those people have said "Well I don't know what to do with this" and never used it again.

And we kind of don't know that with generative AI. So it may be that what we've got now is kind of going to flatten out in the next year or so and what we've got now is kind of it—and it'll improve incrementally and it'll get faster and cheaper, but this is basically the level of capability we're going to have, or maybe a bit more. Or it may be that in 5 years' time we'll all be queuing up to get our ration of gruel from our robot overlords. I'm kind of exaggerating to make the point, but we don't have that same kind of basic theoretical understanding of what this could be.

Moar money

The AI race is incredibly costly:

Elon Musk’s artificial intelligence startup xAI is burning through $1 billion a month as the cost of building its advanced AI models races ahead of the limited revenues, according to people briefed on the company’s financials.

The rate at which the company is bleeding cash provides a stark illustration of the unprecedented financial demands of the artificial intelligence industry, particularly at xAI, where revenues have been slow to materialize. — Bloomberg

My brilliant colleague Pranav recently wrote a comprehensive roundup of the latest developments in AI.

Financial technology has made access to banking services much simpler and has enabled financial inclusion, but it has also created new risks.

Digital banking has made it easier than ever to transfer money, and this is leading to deposits becoming less “sticky.” That means customers are no longer content with low rates and will happily shop around for higher deposit rates, thanks to the ease of transferring money. The question is, what does this reduced deposit stickiness mean for financial stability?

When the Federal Reserve hiked interest rates, deposit growth at traditional banks fell by 7%. At digital banks, deposit growth fell between 11-32%.

Digital banking has enabled smaller banks without branches to attract deposits at a faster pace. But these inflows are often “hot money” flows that flee when economic conditions change.

Digital banks attract depositors by offering higher deposit rates compared to traditional banks. This, however, means that they have to lend at higher interest rates to make money. This is forcing these digital banks to lend for shorter terms to high-risk borrowers.

Digital-forward banks offering high deposit rates now have two distinct challenges, as the researchers document. They need to loan out money at a rate that exceeds the one they are paying depositors, and they need to compensate for the fact that those deposits are.

Bad loans among digital-first banks are three times higher compared to traditional banks.

The Fed's ability to raise rates rapidly is now constrained because digital banking amplifies deposit flight risks.